"THE CASE FOR TWENTY ONE CAPITAL"

A Bitcoin-Native Public Company and Its Strategic Backers

RESEARCH BRIEF

Twenty One Capital: A Bitcoin-Native Public Company and Its Strategic Backers

Introduction

Twenty One Capital is a newly launched Bitcoin-native public company created through a SPAC merger with Cantor Equity Partners. Announced in April 2025, this venture brings together an unusual coalition of crypto and finance heavyweights – Tether, SoftBank Group, Jack Mallers, and Cantor Fitzgerald – each playing a critical role. Twenty One aims to debut on Nasdaq under the ticker “XXI” after merging with the Cantor-sponsored SPAC. What makes Twenty One unique is its plan to start with a massive Bitcoin treasury (~42,000 BTC) and a mission to maximize “Bitcoin Ownership Per Share” for investors. In effect, it seeks to become a pure-play Bitcoin holding company and business builder, positioned as a “superior vehicle” for Bitcoin exposure when compared to existing alternatives like MicroStrategy.

This report analyzes the strategic rationale behind Twenty One’s launch and the implications for the Bitcoin industry. We break down the roles of key players – Tether, SoftBank, Jack Mallers, and Cantor Fitzgerald – examining why each was chosen and what they contribute. We also explore Twenty One’s corporate structure (including its SPAC merger mechanics, PIPE raise, and novel Bitcoin-per-share metrics) and discuss the broader impact: from accelerating institutional Bitcoin adoption and new financial products to shaping the media narrative around crypto. In providing context, we touch on Tether’s expansion into Bitcoin mining (and whether it already runs the largest mining operation), Jack Mallers’ reputation via Strike, SoftBank’s investment motives, and Cantor Fitzgerald’s facilitation role.

A Bitcoin-Native Public Company via SPAC

Twenty One Capital is being formed by merging with Cantor Equity Partners, Inc. (CEP), a special-purpose acquisition company affiliated with Wall Street firm Cantor Fitzgerald. The SPAC route allows Twenty One to go public relatively quickly, raising significant capital in the process. According to the announcement, Twenty One and CEP have lined up $585 million in new funding concurrent with the merger, comprising $385 million in convertible senior notes and $200 million in a PIPE (private investment in public equity). This fresh capital will be used primarily to purchase additional Bitcoin (beyond the founders’ contributions) and for general corporate purposes, enabling Twenty One to launch with over 42,000 BTC on its balance. With that hoard, Twenty One would immediately rank as the third-largest corporate Bitcoin holder globally, behind only Michael Saylor’s company (MicroStrategy) and Marathon Digital Holdings (a major miner).

Structurally, Twenty One is designed from scratch to be a “Bitcoin-native” firm. Unlike MicroStrategy – a legacy software company that pivoted to holding Bitcoin – Twenty One has no legacy business and will focus solely on Bitcoin-related activities. It brands itself as a “public stock, built by Bitcoiners, for Bitcoiners”, signaling its intention to operate with a crypto ethos in a public markets setting. The SPAC merger provides the bridge between the traditional financial market (Nasdaq listing, SEC oversight) and the crypto world (large Bitcoin treasury, industry insiders at the helm). The transaction still requires approval from CEP’s shareholders and regulators, but its announcement alone caused CEP’s stock to soar – shares jumped over 50% on April 23 and continued climbing in after-hours trading, reflecting excitement for this Bitcoin-centric debut.

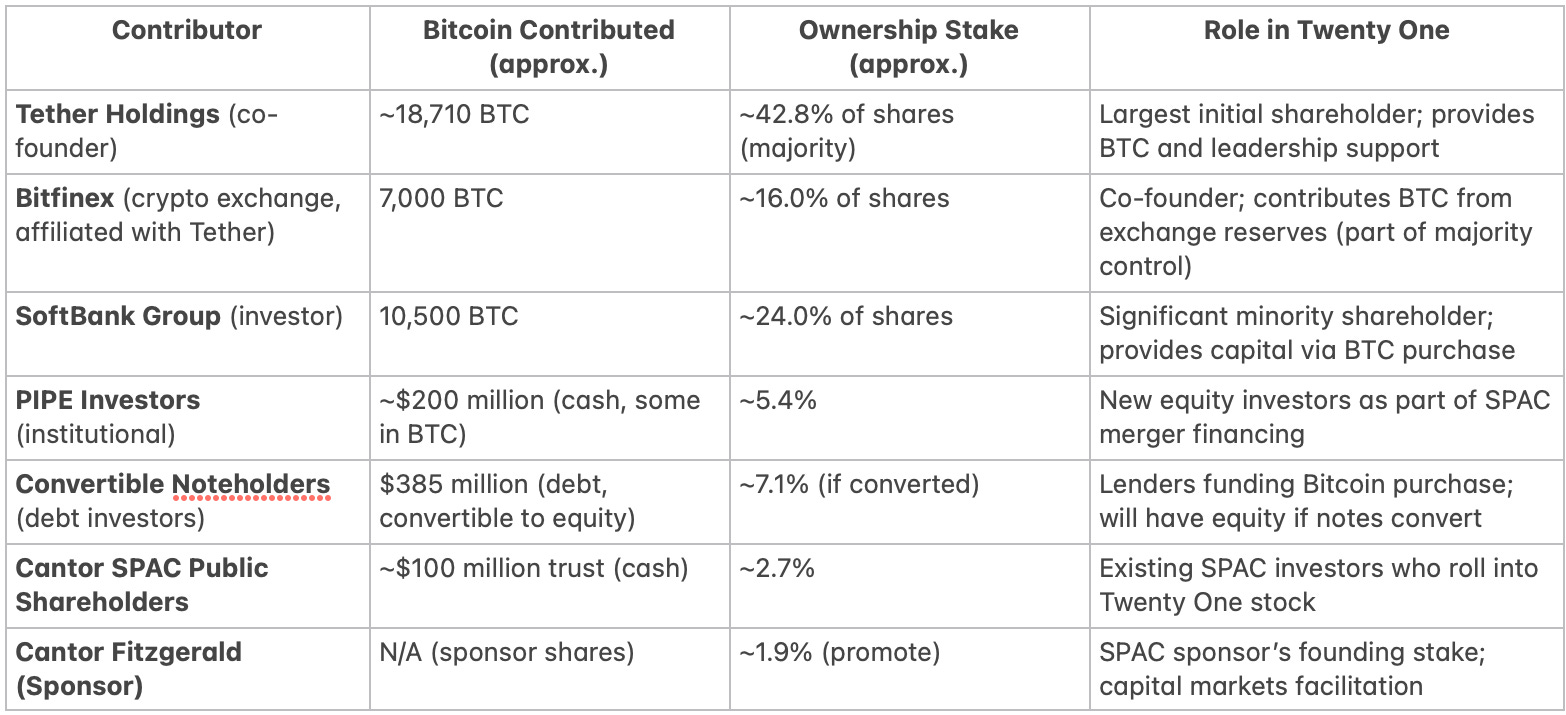

Twenty One’s capital structure at launch will be unusual in that it is heavily Bitcoin-funded. Rather than an all-cash IPO, the founding investors are contributing BTC directly in exchange for equity. In total, roughly 42,000 BTC (worth over $3.5–$3.9 billion at anticipated valuation) will seed the company. Table 1 summarizes the initial sources of Bitcoin and ownership stakes based on filings:

Note: SoftBank’s 10,500 BTC were arranged “on behalf of SoftBank” by Tether prior to closing – essentially, SoftBank committed cash which Tether used to acquire that BTC, to be swapped for SoftBank’s equity at $10/share. Tether and Bitfinex’s holdings include Class A and Class B shares, likely giving them enhanced voting rights (over 50% voting power for Tether alone) to maintain control. This dual-class structure means Tether/Bitfinex will firmly control the company’s direction, aligning with their majority economic stake.

By using BTC contributions and PIPE funding, Twenty One’s valuation is effectively tied to Bitcoin’s net asset value (NAV). The investor presentation noted that PIPE investors are buying in at roughly 1.0× Bitcoin NAV (i.e. paying $1 of share value per $1 of Bitcoin on the books). This is noteworthy because other Bitcoin-holding companies often trade at a premium to their BTC NAV – for example, MicroStrategy’s stock has historically traded higher than the market value of its Bitcoin, reflecting a speculative premium. Twenty One is pitching itself as a more cost-efficient way to buy into Bitcoin via equity, essentially offering early investors a base price that directly reflects the underlying BTC. If successful, this could attract value-conscious crypto investors to the stock.

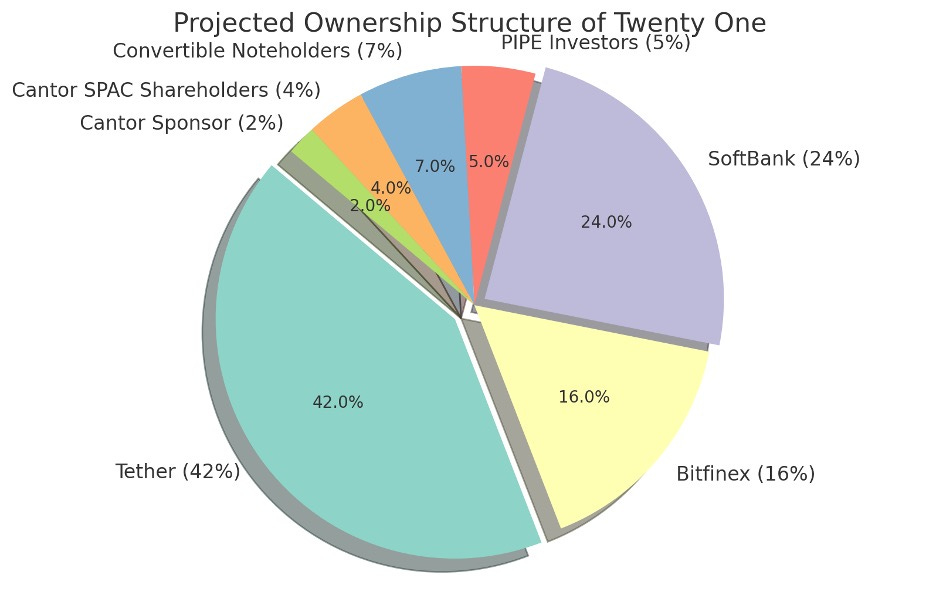

Figure 1: Projected Ownership

Strategic Intent and Purpose of the Venture

Tether’s Ambition: From Stablecoin Giant to Bitcoin Champion

For Tether, the issuer of the world’s largest stablecoin USDT, backing Twenty One Capital is a strategic extension of its long-standing support for Bitcoin. Tether is co-founder and majority owner of Twenty One, contributing the largest share of Bitcoin to the company’s treasury. This move aligns with Tether’s broader vision: it has repeatedly stated that Bitcoin is the “ultimate store of value” and the foundation of a new financial system. By spearheading Twenty One, Tether can directly reinforce Bitcoin’s dominance and utility, which in turn supports the ecosystem in which USDT thrives.

Tether’s strategic intent appears two-fold. First, it seeks to strengthen the Bitcoin ecosystem by investing some of its massive reserves and profits into Bitcoin infrastructure. In 2023, Tether began allocating a portion of profits to buy Bitcoin for its balance sheet and fund initiatives like mining facilities. By end of March 2023, Tether already held about $1.5 billion in BTC as part of its reserves. It then pushed further into Bitcoin mining, investing in renewable energy mining projects in places like Uruguay and El Salvador. Paolo Ardoino, now CEO of Tether, emphasized “harnessing the power of Bitcoin” and using renewable energy, indicating a commitment to Bitcoin’s long-term sustainability. These moves signal that Tether sees Bitcoin as core to the future of crypto – securing and growing the Bitcoin network benefits all of Tether’s business lines (from stablecoins to exchanges).

Second, Tether likely views Twenty One as a way to diversify and legitimize its holdings via public markets. As a private company, Tether has faced skepticism about transparency. By putting a large chunk of Bitcoin into a publicly listed entity, Tether’s assets gain greater visibility and regulatory oversight. It’s telling that Tether chose not to go public directly (which would subject the controversial stablecoin business to scrutiny), but instead to launch a separate vehicle focused purely on Bitcoin. This allows Tether to indirectly participate in public markets upside without exposing its core operations. Twenty One’s success could also bolster confidence in Tether’s financial strength, since Tether will own valuable publicly traded shares and can point to its role in a regulated Bitcoin venture. In essence, Tether is leveraging its financial firepower (from $72+ billion USDT in circulation) to become a major Bitcoin investor – moving beyond just being a liquidity provider to also being a long-term Bitcoin holder and advocate.

From Tether’s perspective, the purpose of Twenty One is very much ideological as well. Tether’s leadership has deep Bitcoin roots (early Tether was issued on the Bitcoin-based Omni layer). Ardoino explicitly stated support for “initiatives that strengthen Bitcoin’s dominance” and praised Twenty One’s Bitcoin-first approach of “prioritizing accumulation over speculation.” This indicates Tether’s intent is not a quick trade or publicity stunt – it’s a strategic commitment to Bitcoin’s future. By co-founding Twenty One, Tether can drive the narrative of Bitcoin in public markets (countering critics with a positive example of a Bitcoin-focused company) and ensure that at least one public entity remains uncompromisingly pro-Bitcoin. This dovetails with Tether’s own survival strategy: as regulators eye stablecoins, Tether is shoring up influence in the one asset (BTC) that is beyond any central authority’s control. In short, Tether is using Twenty One to cement its role as a pillar of the Bitcoin ecosystem, spanning everything from mining to treasury management to public-market advocacy.

SoftBank’s Bet: A Major Investor Embraces Bitcoin’s Upside

SoftBank Group’s involvement brings a high-profile stamp of mainstream credibility to Twenty One. SoftBank, a Japanese conglomerate known for its $100+ billion Vision Fund and big bets on technology companies, is taking a significant minority stake in Twenty One. It is contributing the equivalent of 10,500 BTC (valued around $800–900 million in the deal) for roughly 24% ownership. For SoftBank, which historically invested in e-commerce, fintech, and internet startups, this move represents a strategic pivot into the Bitcoin sector.

The timing and structure of SoftBank’s bet suggest a broader strategic intent to capture what it sees as a generational opportunity in Bitcoin. Over the past few years, institutional attitudes toward Bitcoin have shifted from skepticism to cautious interest – and by 2025, factors like high inflation and geopolitical uncertainty have boosted Bitcoin’s appeal as an alternative asset. SoftBank’s investment thesis likely aligns with Twenty One’s: that Bitcoin is entering a phase of widespread adoption by institutions and even governments, with improving regulatory clarity, making now a prime time to invest. Unlike buying Bitcoin outright, joining Twenty One gives SoftBank exposure to Bitcoin’s upside plus a say in building new Bitcoin businesses (via board influence, etc.). In essence, SoftBank likely sees Twenty One as a “Bitcoin holding company” that can grow faster than Bitcoin itself by leveraging strategic capital raises and ventures. This is akin to how SoftBank might invest in a gold ETF provider rather than just gold, hoping the company’s activities generate extra return on top of the asset’s price.

SoftBank’s decision to partner with Tether and Jack Mallers in this SPAC also reveals something about why they were selected. SoftBank is no stranger to crypto – it invested in the FTX exchange (and infamously had to write down ~$100 million after FTX’s collapse). That experience, and others, likely taught SoftBank to favor Bitcoin-focused opportunities over broader crypto speculation. By backing a Bitcoin-only firm with substantial physical BTC backing (42,000 coins), SoftBank reduces the risk of investing in a single startup or token. The presence of Tether (a highly profitable company) and Bitfinex as majority owners likely gave SoftBank confidence that Twenty One will have strong support and liquidity. In fact, Tether even facilitated SoftBank’s BTC purchase for the deal, indicating close cooperation. SoftBank’s global influence and deep pockets make it an ideal partner – it can provide follow-on capital, open doors to international markets, and lend Board-level guidance. SoftBank also tends to invest in market leaders; by joining forces with Tether (the leader in stablecoins) in a Bitcoin venture, SoftBank positions itself at the forefront of institutional Bitcoin adoption, rather than on the sidelines.

Another angle to SoftBank’s involvement is the media and investor signaling effect. SoftBank’s founder Masayoshi Son is known for his visionary (if sometimes risky) bets – from Alibaba to Arm to Uber. A public endorsement of Bitcoin via Twenty One signals to other large investors that Bitcoin is now a serious institutional asset class. It’s quite notable considering Son once admitted he didn’t understand Bitcoin and sold his personal BTC at a loss years ago; now SoftBank is embracing a Bitcoin-native enterprise. This evolution in stance could influence peers (other VCs, sovereign wealth funds, etc.) to reevaluate Bitcoin opportunities. In summary, SoftBank’s rationale appears to be diversification into what it sees as “the most valuable financial opportunity of our time” (to quote Mallers’ description of Bitcoin) – capturing upside from Bitcoin’s growth while partnering with industry experts to mitigate the execution risks.

Jack Mallers: A Bitcoin Evangelist at the Helm

Jack Mallers – best known as the founder and CEO of Strike, a Bitcoin Lightning payments company – will serve as Twenty One’s co-founder and CEO. Mallers’ appointment to lead Twenty One is strategic: he brings deep Bitcoin expertise, industry credibility, and a passionate vision to the venture. In the Bitcoin community, Mallers, still in his late 20s, has a reputation as an outspoken evangelist for using Bitcoin as a currency (via Lightning Network) and as a long-term store of value. He rose to prominence by helping facilitate El Salvador’s historic decision to adopt Bitcoin as legal tender in 2021 – Mallers and Strike were instrumental in that rollout. He has also brokered partnerships to integrate Bitcoin Lightning payments with major players like Visa, Shopify, and fintech firms. In short, Mallers has been a key figure in Bitcoin’s evolution from an investment commodity to a usable financial network.

By selecting Mallers as CEO, Twenty One’s backers ensured the company is “built by Bitcoiners” at its core, not just managed by traditional financiers. Mallers’ presence signals to the Bitcoin community that Twenty One is authentic and mission-driven. This is important because Bitcoin purists can be skeptical of Wall Street or corporate initiatives that might “co-opt” Bitcoin. With Mallers at the helm, Twenty One gains trust and goodwill among Bitcoin enthusiasts – a base of support that can be valuable for everything from talent recruitment to customer acquisition for any products they launch. Moreover, Mallers is known for a fiery, evangelical communication style (for example, his energetic speeches at Bitcoin conferences). As CEO of a public company, he can carry that message to a broader audience, making the case for Bitcoin on earnings calls and media interviews. This combination of technical knowledge and evangelism is something neither Tether nor SoftBank alone could provide; Mallers fills that role.

Strategically, Mallers also bridges the gap between startup innovation and public market discipline. He will continue as CEO of Strike while leading Twenty One, which suggests potential synergies. Strike’s experience in Bitcoin payments and infrastructure could inform Twenty One’s planned financial products. It’s conceivable that Twenty One might partner with, invest in, or even acquire businesses like Strike in the future (Mallers’ dual role at least fosters alignment). His influence in both companies means Twenty One’s strategy won’t be just about passive Bitcoin holding – it will be guided by someone actively building on Bitcoin technology. This is crucial for Twenty One’s goal to do more than “just stack sats.” As Mallers said, “We’re not here to beat the market, we’re here to build a new one”. That ethos reflects an ambition to create new Bitcoin-native markets and products, not merely ride Bitcoin’s price.

In summary, Jack Mallers brings visionary leadership and Bitcoin ethos to Twenty One. He was likely chosen because he personifies the idea of a “Bitcoin-native” entrepreneur who can articulate the long-term value of Bitcoin to both retail investors and institutions. His strategic importance cannot be overstated: with Mallers as CEO, Twenty One has a figurehead who is respected by hardcore Bitcoiners and able to engage with Wall Street on Bitcoin’s terms. This blending of cultures – crypto-native and traditional finance – is exactly what Twenty One wants to achieve. Mallers gives the venture a human face and a guiding philosophy centered on Bitcoin adoption, innovation, and advocacy.

Cantor Fitzgerald’s Role: SPAC Sponsor and Bridge to Wall Street

Cantor Fitzgerald, through its affiliate Cantor Equity Partners, is the sponsor and facilitator of Twenty One’s journey to the public market. Cantor Fitzgerald is a venerable Wall Street institution (founded in 1945) with expertise in brokerage, investment banking, and more recently SPACs and fintech. In this deal, Cantor’s SPAC provides the “blank check” vehicle (ticker: CEP) that Twenty One will merge into. Cantor’s chairman and the CEO of the SPAC, Howard Lutnick, described the collaboration between “Tether, a foundation for today’s digital asset ecosystem, and SoftBank, one of the world’s preeminent investors” as an “extraordinary” opportunity. This statement underscores Cantor’s view of itself as the bridge between innovative crypto players and big institutional capital.

As the SPAC sponsor, Cantor’s primary role was to identify a suitable target and negotiate the merger and financing terms. Given Cantor’s existing relationship with Tether – Cantor actually manages a portion of the US Treasury reserves backing USDT and even owns a 5% equity stake in Tether’s parent – it’s no surprise they were the matchmaker for Twenty One. Cantor likely approached Tether with the SPAC idea, knowing Tether’s interest in expanding Bitcoin holdings. Their existing trust (managing billions in Tether’s reserves) would have smoothed negotiations. For Cantor, this deal is a marquee transaction that leverages its capital markets expertise in a novel way. They arranged the PIPE and convertible note financing, tapping their network of institutional investors to raise the $585 million. They also contributed $45 million via the sponsor unit as a convertible note, aligning their interests in the company’s success.

Cantor Fitzgerald’s involvement brings crucial regulatory and operational know-how to Twenty One. Navigating SEC requirements, stock exchange rules, and SPAC shareholder approvals can be complex – having an experienced partner like Cantor is invaluable. Additionally, Cantor will likely remain an advisor or market-maker for Twenty One post-listing, ensuring the stock’s liquidity and helping structure any future debt or equity raises. Essentially, Cantor acts as the gateway to Wall Street, translating Twenty One’s Bitcoin vision into a language traditional investors understand. Their investor presentation, filed with the SEC, carefully compares Twenty One to MicroStrategy and highlights metrics like NAV multiples to appeal to value investors – a very Cantor-esque approach to framing the crypto opportunity in conventional financial terms.

Why was Cantor selected? Apart from the prior ties to Tether, Cantor has a history of interest in digital assets. Back in 2017–2018, Cantor Fitzgerald was among the first finance firms looking into Bitcoin derivatives and even planned a Bitcoin futures exchange. While those early plans didn’t fully materialize, Cantor signaled openness to crypto innovation. By 2025, after the ups and downs of the crypto market, Cantor likely saw Twenty One as a way to reassert itself as a forward-thinking firm in the fintech space. Many SPAC sponsors had shied away from crypto deals after some high-profile failures (for instance, Circle’s SPAC merger was called off in 2022 amid regulatory delays). Cantor stepping up to sponsor Twenty One demonstrates a conviction that a Bitcoin-focused company can succeed in the public market – provided it has the right structure and backers. Cantor’s reward is a small equity stake (~1.9% post-merger) and the fees from arranging the deal, but perhaps more importantly, a lead role in one of the most notable crypto financings of the year. In sum, Cantor Fitzgerald’s role is that of facilitator and validator: it gave Twenty One the vehicle and legitimacy to attract large capital, and it will help steer the venture through the intricacies of the public markets.

Twenty One’s Structure and Bitcoin-Centric Strategy

From day one, Twenty One Capital is structured to maximize its alignment with Bitcoin. The company’s balance sheet and performance metrics are denominated in BTC, reflecting an almost unprecedented approach to corporate finance. Rather than measure success in earnings per share (EPS) in dollars, Twenty One will measure it in “Bitcoin per share” (BPS) – literally how much BTC each share represents. At launch, given ~42,000 BTC and the planned share count, the initial BPS will be determined (for example, if there are ~370 million diluted shares, BPS might be around 0.000113 BTC/share). The goal is to grow that BPS over time, meaning each share should entitle investors to more and more satoshis as the company accumulates additional Bitcoin. They have even introduced a “Bitcoin Return Rate (BRR),” defined as the rate at which BPS grows. This essentially reframes the company’s ROI in Bitcoin terms, emphasizing that management’s job is to increase Bitcoin holdings faster than just holding BTC passively would. These metrics underscore Twenty One’s philosophy: shareholder value = Bitcoin accumulation. In other words, the company is aligning investor interests with the core Bitcoin mantra of “stacking sats.”

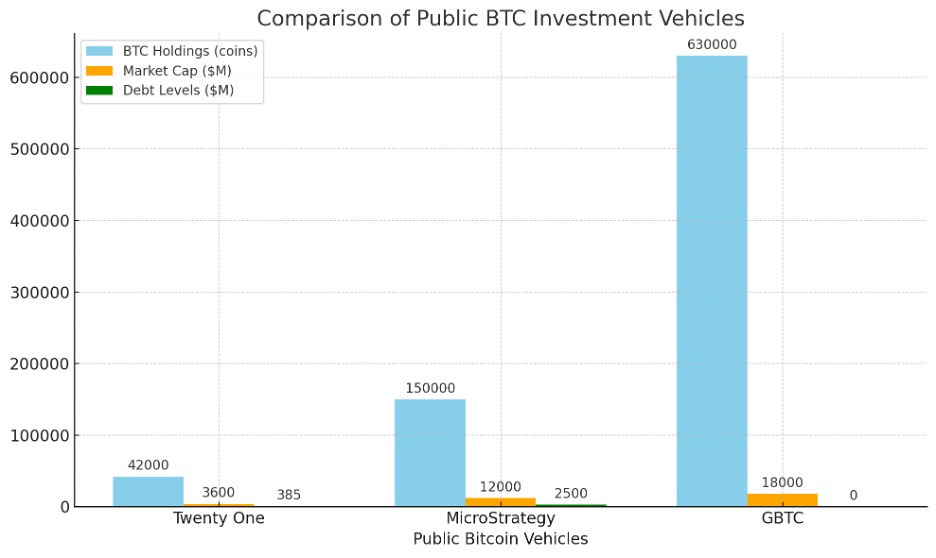

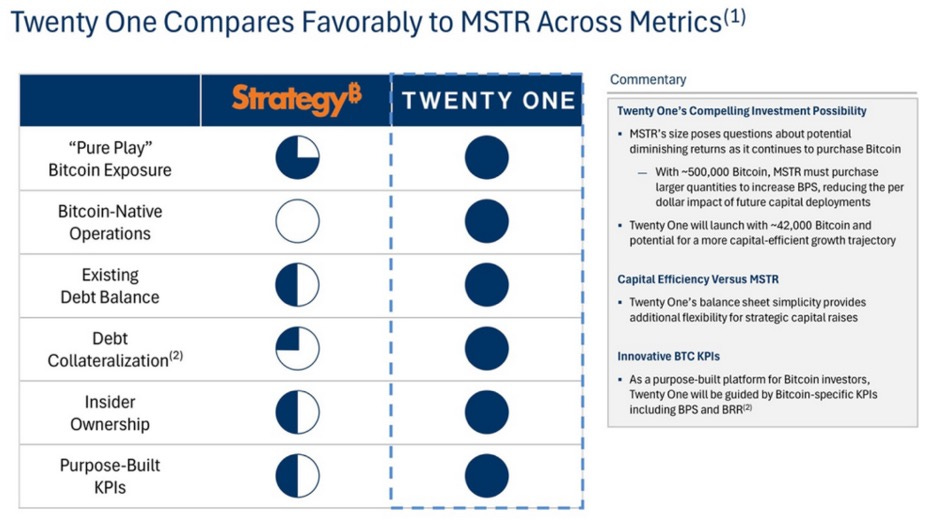

Figure 2: Comparison Public BTC Investment Vehicles

To achieve growth in BPS, Twenty One’s structure combines active treasury management with operating businesses. The $585 million in new capital will immediately boost the BTC treasury (likely adding 5,000+ BTC on top of the founders’ 37,500 BTC, to reach the 42,000+ BTC total). Beyond that, the company plans to use part of its Bitcoin to generate returns for shareholders. This could involve yield strategies like lending Bitcoin or using it as collateral to raise low-cost debt (taking advantage of its pristine asset status). Unlike MicroStrategy, which is constrained by having to service large debts and continually issue equity to buy more BTC, Twenty One starts with a clean balance sheet (no legacy debt) and a significant war chest. This gives it flexibility to pursue opportunistic raises or investments without diluting BPS too quickly. In fact, the investor deck favorably contrasts Twenty One’s simplicity to MicroStrategy’s situation – MicroStrategy’s very large existing holdings (>150,000 BTC) mean any new purchase has a diluted impact on its per-share metrics. Twenty One, with a smaller initial base and fresh capital, argues it has a “more capital-efficient growth trajectory” for Bitcoin per share.

Figure 3: Twenty One Capital’s investor presentation compares its attributes to MicroStrategy’s “Strategy❜” (Michael Saylor’s Bitcoin-heavy firm). Twenty One pitches itself as a purer Bitcoin play with no existing non-Bitcoin business, no burdensome debt, and purpose-built Bitcoin KPIs like BPS and BRR. By launching with ~42k BTC and focusing on Bitcoin-native operations, Twenty One claims it can increase Bitcoin-per-share more efficiently than a large incumbent can.

In terms of corporate structure, Twenty One will have a dual-class share setup (e.g. Class A and Class B shares) to keep control in the hands of Tether/Bitfinex and potentially Jack Mallers. The ownership table (Table 1) shows Tether and Bitfinex collectively with ~59% of shares but an even higher voting percentage (over 70% combined votes, with Tether alone around 52% vote). This indicates that Class B shares with super-voting rights were likely issued to the founders. Such a structure is common in founder-led tech companies, allowing them to pursue long-term strategy (in this case, a Bitcoin accumulation strategy) without fear of activist investors or hostile takeovers. For Twenty One, this means Mallers and Tether can prioritize Bitcoin growth over short-term profits without as much pressure from minority shareholders. It aligns with their motto of building “long-term value for those who understand what Bitcoin represents.”

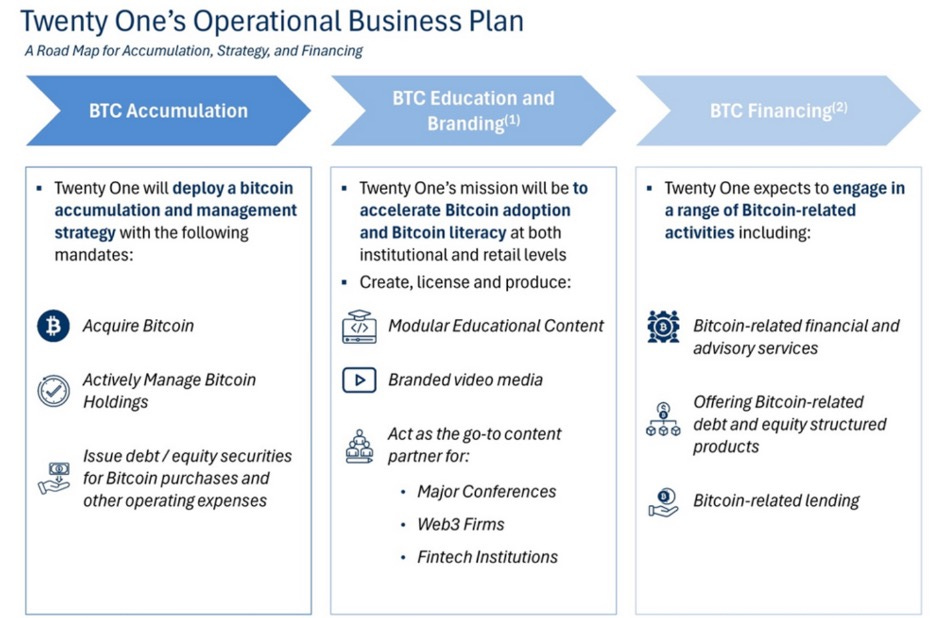

While holding BTC is the cornerstone, Twenty One’s strategy extends into building Bitcoin-centric businesses for additional value. According to the company’s plan, there are three primary pillars for operations: Bitcoin accumulation, Bitcoin education/branding, and Bitcoin financial services. These were outlined in an operational roadmap:

Figure 4: Twenty One Capital’s operational business plan has three prongs – (1) BTC Accumulation, involving active treasury management and raising capital to acquire Bitcoin; (2) BTC Education & Branding, to promote Bitcoin literacy via content, media, and events; and (3) BTC Financing, which includes Bitcoin-related financial and advisory services, lending, and structured products. This illustrates that Twenty One isn’t just a static BTC holding company, but also aims to be an active builder of Bitcoin infrastructure and knowledge.

Concretely, Twenty One plans to offer or develop:

Bitcoin-denominated debt and equity products – for example, bonds or loans where interest/principal are in BTC, or investment products for others to gain Bitcoin exposure. This could make Twenty One something of a Bitcoin investment bank, structuring instruments for institutions that want Bitcoin yields or financing.

Advisory services for Bitcoin adoption – acting as consultants to corporations or even governments on how to integrate Bitcoin into their treasuries (much like how Jack Mallers advised El Salvador). This leverages Mallers’ and Tether’s experience in guiding large entities into Bitcoin.

A Bitcoin lending platform – which might involve lending out Bitcoin to earn yield or offering Bitcoin-backed loans to others. This would compete with (or replace) the likes of BlockFi/Celsius but in a presumably more regulated, transparent manner under a public company.

Educational and media initiatives – Twenty One explicitly intends to produce original content, run major Bitcoin conferences in partnership with others, and generally be a loud advocate for Bitcoin in public discourse. This could entail publishing research, running a media site or video series, and using its platform to influence policy and public opinion in favor of Bitcoin.

The inclusion of an education/media arm is particularly interesting. It suggests Twenty One sees part of its mission as shaping the narrative around Bitcoin. With the backing of Tether and SoftBank, they could fund high-quality documentaries, courses, or events that highlight Bitcoin’s benefits and dispel myths. Essentially, Twenty One might become a pro-Bitcoin think tank or media outlet alongside being an operating company. This is a strategic choice: a more informed public and institutional base will likely lead to greater Bitcoin adoption, which ultimately benefits Twenty One’s holdings and business prospects. It’s also a differentiator – MicroStrategy’s advocacy is mostly via Michael Saylor’s interviews, whereas Twenty One could institutionalize the advocacy via formal content channels.

Financially, the structure of raising both equity (PIPE) and convertible notes is designed to balance growth and risk. The $385 million convertible notes give the company cash now to buy BTC, but defer equity dilution into the future (noteholders likely can convert to shares only if the stock rises above a certain price). This indicates confidence from investors that Twenty One’s stock could appreciate – possibly if Bitcoin’s price increases or if the company’s activities generate additional value. The notes are senior secured, meaning they have claims on assets (presumably BTC) if something goes awry, which gave note investors downside protection. From Twenty One’s perspective, this is smart leverage: borrowing against Bitcoin at presumably low interest to acquire more Bitcoin upfront. If Bitcoin’s price goes up, the company benefits equity holders; if it stays flat, the cost is just the interest and eventual dilution. This approach mirrors MicroStrategy’s playbook of issuing convertible bonds to buy BTC, but Twenty One is doing it from inception, highlighting its aggressive stance on accumulation.

In summary, Twenty One’s structure is all about maximizing Bitcoin accumulation per share while building complementary revenue streams around Bitcoin. By measuring performance in BTC terms (BPS, BRR), it aligns management with Bitcoin-minded investors. The combination of an initially large BTC treasury, flexible capital structure, and plans for Bitcoin-native products suggests Twenty One will function as a hybrid of a Bitcoin ETF, a Bitcoin bank, and a Bitcoin media company. If executed well, this structure could yield a company whose value grows not only with the price of Bitcoin, but also through the cash flows of Bitcoin-focused services – creating a virtuous cycle to further “accelerate Bitcoin adoption,” as the firm’s mission states.

Implications for the Bitcoin Industry

Accelerating Institutional Adoption

The launch of Twenty One Capital is a strong indicator that institutional adoption of Bitcoin is entering a new phase. By involving a major investment conglomerate (SoftBank) and a Wall Street firm (Cantor) alongside crypto natives, Twenty One bridges worlds that were previously separate. This has several implications:

First, it provides a template for other institutions to get involved in Bitcoin through creative means. If Twenty One proves successful, we may see more “Bitcoin SPAC” deals or similar structures where traditional investors team up with crypto firms. Institutional treasurers and fund managers will be watching how Twenty One performs. A positive track record could spur copycat strategies: for instance, other large investors might attempt to launch their own Bitcoin holding companies or push existing public companies to allocate to Bitcoin. The fact that SoftBank – known for its exhaustive due diligence and risk assessment – is investing heavily sends a message that Bitcoin exposure is now a legitimate component of a modern portfolio (whereas a decade ago it was seen as wildly speculative). This could normalize Bitcoin investment at the boardroom level. We could see more pension funds, endowments, or corporates allocate indirectly via Twenty One or similar vehicles, thus broadening institutional ownership of BTC.

Second, Twenty One’s focus on being the “superior vehicle” for Bitcoin exposure challenges existing avenues and may drive improvements across the industry. Bitcoin ETFs (exchange-traded funds) have been one popular proposed avenue for institutions, and by 2025 several ETFs either exist or are pending approval. However, an ETF only tracks Bitcoin’s price; Twenty One offers a potentially leveraged exposure (through business activities and strategic raises). If Twenty One trades at a premium to NAV because investors value its growth potential, that indicates appetite for managed Bitcoin exposure rather than purely passive holding. This could encourage ETF issuers or fund managers to consider more active or hybrid approaches (for example, ETFs that also lend out Bitcoin for yield). In the meantime, Twenty One gives institutions an immediate publicly traded option – it can be bought on Nasdaq like any stock, circumventing certain restrictions that might prevent direct crypto purchases. Public market exposure via equities can thus increase. We might even see mutual funds or ETFs that hold Twenty One’s stock as a proxy for Bitcoin. In the same way GBTC (Grayscale Bitcoin Trust) served as a proxy in the past, Twenty One could become a new bellwether stock for Bitcoin sentiment.

Furthermore, Twenty One’s positioning may influence regulatory perspectives. Seeing a compliant, fully-reporting U.S. public company built around Bitcoin could alleviate some regulatory concerns by demonstrating that Bitcoin can be integrated into the traditional financial system with proper oversight. If the SEC sees Twenty One successfully list and function, it undercuts arguments that Bitcoin markets are “unready” for mainstream products. On the other hand, regulators will likely scrutinize Twenty One’s disclosures, risk factors (volatility, custody of BTC, etc.), and internal controls, potentially setting new standards for Bitcoin risk management in public companies. Institutional adoption isn’t just about buying – it’s about adapting frameworks to accommodate Bitcoin. Twenty One will be a high-profile test case, and positive outcomes (no major custody losses, clear audits of BTC holdings, etc.) will pave the way for more institutions to follow.

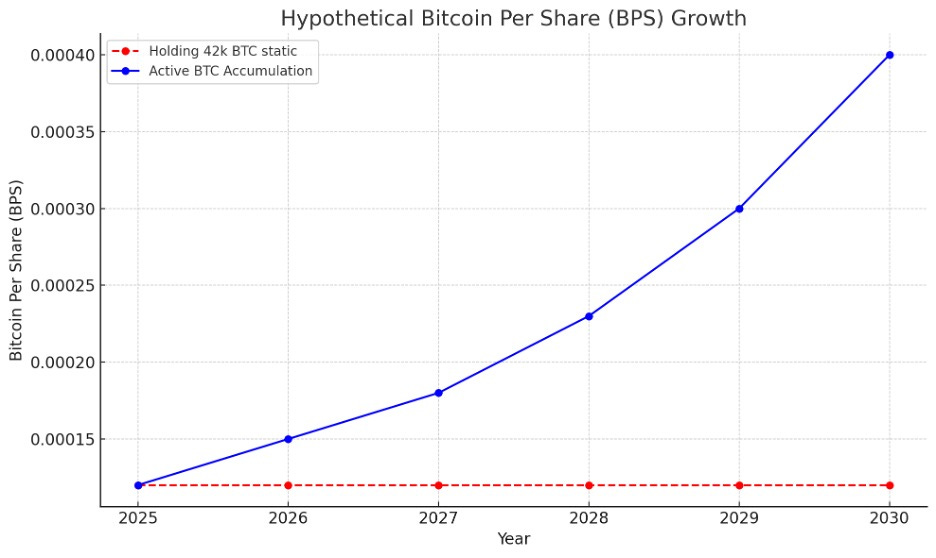

Figure 5: Hypothetical Bitcoin Per Share (BPS) Growth

New Bitcoin Financial Products and Services

The creation of Twenty One is likely to spur innovation in Bitcoin-backed financial products. Twenty One itself plans to roll out products like Bitcoin-backed loans, Bitcoin-denominated bonds, and other structured products. This could have a competitive and demonstrative effect across the industry:

Bitcoin Collateralized Lending: If Twenty One launches a robust lending platform (perhaps targeting institutions or high-net-worth individuals who want to borrow against their Bitcoin), it could standardize practices for Bitcoin collateral management. Unlike the earlier generation of crypto lenders that often engaged in risky rehypothecation, a publicly traded Twenty One would need prudent risk controls. Successful Bitcoin lending by Twenty One might encourage traditional banks to dip their toes in (using Bitcoin as collateral for loans to corporate clients, for example). It also pressures existing crypto lenders to up their game on transparency and risk management. In general, more availability of credit against Bitcoin holdings increases Bitcoin’s utility for investors, potentially drawing in those who want to hold BTC but still access liquidity.

Debt and Equity Instruments: Twenty One’s mention of Bitcoin-related debt/equity structured products suggests things like Bitcoin yield notes, convertible bonds tied to Bitcoin performance, or even Bitcoin-backed annuities. These kinds of instruments could open Bitcoin investment to more conservative profiles. For example, an insurance company might not buy BTC outright, but it might buy a bond issued by Twenty One that pays interest linked to Bitcoin’s price. By pioneering such products, Twenty One can expand the Bitcoin financial derivatives market. We may see others follow suit: perhaps Bitcoin mining companies issuing revenue bonds, or traditional firms issuing Bitcoin-linked bonds to raise money for BTC purchases. The market infrastructure for pricing and trading Bitcoin-linked credit will grow. It also intertwines Bitcoin with traditional capital markets – once you have many bonds and loans dependent on Bitcoin’s value, there’s a vested interest in seeing Bitcoin succeed and a push for clearer pricing and lower volatility.

Bitcoin Insurance and Services: Twenty One’s holistic approach (including advisory and education) could give rise to an ecosystem of services around Bitcoin for institutions. If they advise a Fortune 500 company on putting Bitcoin in its treasury, that involves legal, accounting, and custodial frameworks. As Twenty One develops these playbooks, it essentially acts as a consultant/clearinghouse for institutional Bitcoin adoption. Others in the industry (big four audit firms, insurance underwriters for crypto custody, etc.) will learn from these cases, and their comfort with Bitcoin will increase. In effect, Twenty One might help hammer out standard practices for things like Bitcoin accounting (an area that has been contentious under GAAP rules), or how to hedge Bitcoin exposure for corporates. This knowledge spills over and benefits the wider industry by reducing frictions that currently make institutions hesitate.

Competition with Traditional Crypto Firms: Twenty One’s emergence also puts competitive pressure on crypto-native firms like Coinbase, Galaxy Digital, or even MicroStrategy. For instance, if Twenty One offers Bitcoin custody or yield products at scale, exchanges like Coinbase might have to respond by enhancing their institutional offerings. MicroStrategy, which so far only buys and holds, could feel pressure to do more (perhaps monetizing its holdings via covered calls or lending, which Saylor has largely avoided). Even stablecoin issuers like Circle (USDC) might note Tether’s moves and consider similar tie-ins with Bitcoin to differentiate themselves. Overall, Twenty One’s product suite could push the industry toward more interconnected crypto financial markets, where Bitcoin is not just an investment asset but a cornerstone of new financial engineering.

Shaping the Media Narrative and Public Perception

The collaboration behind Twenty One is tailor-made to generate media interest – and likely a favorable narrative – about Bitcoin. In the mainstream media, stories about Bitcoin often focus on volatility, regulatory crackdowns, or speculative mania. Twenty One offers a different narrative: one of serious businesspeople and firms coming together to build a regulated, institutional-grade Bitcoin company. This has a few implications:

Legitimizing Bitcoin via High-Profile Endorsement: When names like SoftBank and Cantor Fitzgerald are attached to a Bitcoin venture, it grabs the attention of financial media in a way pure crypto startups do not. The fact that SoftBank (which also famously backed Alibaba) is involved provides a comparison that media can latch onto – e.g., “Is Bitcoin the next big bet for SoftBank?” This can shift the narrative from “Bitcoin as a fringe asset” to “Bitcoin as the next frontier of innovation that even big banks and funds are pursuing.” Similarly, Jack Mallers’ involvement gives the crypto press a hero figure to write about, framing him as a young visionary leading Wall Street into Bitcoin. We’ve already seen headlines highlighting that Mallers aims to “dethrone Michael Saylor’s strategy”, which casts Twenty One as a bold challenger and keeps the story in a positive, competitive light (as opposed to regulatory or scandal-focused coverage).

Media & Content as Part of Strategy: Since Twenty One explicitly will produce Bitcoin-focused content and possibly host conferences, it is in a position to directly influence the narrative. They could sponsor documentaries on Bitcoin’s societal impact, publish educational series for CNBC/Bloomberg, or host summits that attract journalists and policymakers. In doing so, Twenty One acts almost like a PR agency for Bitcoin (with the credibility of a public company). This proactive approach can help counter misinformation. For example, if there are renewed environmental FUD (fear, uncertainty, doubt) about Bitcoin mining, Twenty One – backed by Tether’s mining data – can put out authoritative content on renewable mining and efficiency improvements. Over time, such efforts can improve public understanding of Bitcoin’s positives (financial inclusion, sound money principles, technological innovation) and mitigate the negatives in discourse.

Changing the Conversation from Speculation to Infrastructure: Twenty One’s messaging (as seen in Mallers’ and Ardoino’s quotes) is about building and accumulating, not trading. This emphasizes Bitcoin as a long-term value play and infrastructure for a new economy, rather than a short-term trade. If the media picks up on that, we may see more stories framing Bitcoin as “digital gold 2.0” or “the base layer of future finance” – narratives that have been gaining traction but will be reinforced by prominent figures in Twenty One repeating them. Additionally, Tether’s involvement allows discussion of the symbiosis between stablecoins and Bitcoin, possibly leading to a more nuanced narrative that the crypto ecosystem is professionalizing.

Public Market Scrutiny Bringing Transparency: A side effect of Twenty One going public is that it will have to disclose a lot of information – risk factors, audited financials, business strategies – in SEC filings. Journalists and analysts will comb through these. Assuming Twenty One maintains high transparency (e.g., proving its BTC reserves, revealing its strategies), it sets a benchmark that can make the entire Bitcoin space seem more transparent. Tether, which has often been criticized for opaque reserves, indirectly benefits if Twenty One is seen as an open book (given Tether’s majority stake, any positive light on Twenty One somewhat shines on Tether too). The media might shift from asking “Does Tether really have the dollars it claims?” to noting “Tether and partners have put billions in Bitcoin into a fully reported entity.”

In short, Twenty One is likely to drive a more mature media narrative about Bitcoin – one centered on big investments, strategic moves, and innovation, rather than just price speculation or crime. This can influence the public perception of Bitcoin, making it easier for an average person to see Bitcoin as something that serious companies and investors believe in for the long haul. A change in narrative can have feedback effects: better perception can lead to friendlier regulation and more adoption, which again improves perception. Twenty One’s very existence as a public company means Bitcoin news will increasingly be reported on financial tickers (stock up or down) rather than only on crypto blogs, integrating Bitcoin into the fabric of financial news.

Public Market Exposure and Investor Access

Before Twenty One, investors seeking exposure to Bitcoin through public markets had a limited menu: they could buy shares of MicroStrategy (MSTR), invest in Bitcoin mining stocks (like Marathon, Riot, etc.), or use crypto trusts/ETPs (like Grayscale’s GBTC, which often traded at a premium or discount). Twenty One’s arrival changes that landscape by providing a new kind of vehicle – one that combines the large Bitcoin holdings of a MicroStrategy with the growth aspirations of a fintech startup.

The implications for investors are significant. With ticker “XXI” planned on Nasdaq, essentially any stock investor globally will be able to add Twenty One to their portfolio to get Bitcoin exposure. This can widen the base of Bitcoin investors beyond those comfortable buying crypto directly. Notably, Twenty One is positioning itself as a more pure and leveraged Bitcoin play than MicroStrategy:

MicroStrategy has around 150k BTC but also a legacy software business and over $2 billion in debt; its stock performance can be impacted by those factors and its large share issuance over time. Twenty One will have a cleaner focus and potentially faster growth in BTC per share (since it can issue shares at NAV to buy more BTC when advantageous, something MicroStrategy can’t easily do without affecting its premium).

Mining stocks provide leveraged Bitcoin exposure (their earnings and stock prices often move more than Bitcoin’s price), but they carry operational risks like energy costs, regulatory issues, and miner delivery delays. Twenty One offers a different kind of leverage: financial leverage and strategic leverage rather than operational. Investors bullish on Bitcoin but wary of the mining sector might prefer Twenty One as a safer bet, knowing its BTC aren’t being sold to cover expenses (since it’s well-capitalized) and it can even earn yield on its BTC.

This new option could impact how capital flows into the Bitcoin space. For instance, crypto ETFs and funds might buy into Twenty One if it trades at a good value relative to its BTC (some fund managers in the past bought MicroStrategy or GBTC in lieu of direct BTC). Also, retail investors who use brokerage apps can diversify into Bitcoin by buying XXI shares without needing a crypto exchange account. The more Bitcoin is baked into conventional investment channels, the more interconnected traditional markets and crypto markets become. We might see correlation effects: if Bitcoin price surges, not only does MicroStrategy stock rally, but now Twenty One’s will too, possibly amplifying momentum as momentum investors pile into these proxies. Conversely, Bitcoin downturns will be transmitted to more stock portfolios via these companies, meaning volatility management and hedging in the broader market might start accounting for Bitcoin.

Public market exposure via Twenty One also means increased scrutiny and analysis from equity analysts. We may see analysts from big banks initiate coverage on Twenty One, thereby indirectly covering Bitcoin. They’ll project Bitcoin price scenarios and business revenue forecasts, effectively bringing Bitcoin discussions into stock analyst reports. This helps integrate Bitcoin into frameworks that equity investors use, potentially reducing the “mystery” or “exotic” aura that might deter some investors.

Lastly, Twenty One’s public listing could encourage other crypto firms to consider the SPAC or IPO route again. If this SPAC is well-received (as the initial stock pop indicated) and maintains investor interest, it could revive crypto SPAC deals which had cooled off. We might see other Bitcoin-heavy firms (for example, large mining firms or crypto platforms) attempt similar mergers or IPOs, riding on Twenty One’s coattails. Each successful listing adds liquidity and maturity to the crypto equity sector, which in turn makes indexes or ETFs of crypto stocks more viable. Over time, one can envision a whole category of “Bitcoin-operating companies” as a subset of the market, much like gold mining companies exist alongside gold ETFs.

Tether’s Mining Operations and Connection to Twenty One

One intriguing aspect of this story is Tether’s foray into Bitcoin mining and how it might tie into Twenty One’s future. Tether has indeed become a significant player in Bitcoin mining recently – though it’s a stretch to say it “already owns the largest bitcoin mining operation,” it is certainly aiming for a top spot. In mid-2023, Tether announced a $500 million investment to build sustainable Bitcoin mining capacity in Uruguay, Paraguay, El Salvador and other locations. By the end of 2023, Tether projected reaching 120 megawatts of mining power, and a whopping 450 MW by end of 2025. For context, 450 MW could support roughly 150,000 of the latest mining rigs, potentially yielding on the order of 5–10 exahashes per second of hash rate – a substantial chunk of the Bitcoin network. Tether also joined El Salvador’s Volcano Energy project, a planned 241 MW renewable-powered Bitcoin mine, providing capital and expertise. These moves indicate Tether is rapidly expanding its mining footprint, possibly putting it on track to be among the world’s largest Bitcoin miners within a couple of years.

How does this connect to Twenty One? The synergy is clear: Tether’s mining operations will generate new Bitcoin, and Twenty One’s mission is to accumulate Bitcoin. It would make sense for Twenty One to have arrangements with Tether to acquire some of that mined Bitcoin. In fact, part of the SPAC plan involved Tether doing “interim funding” to buy 5,440 BTC (worth $462M) before closing, which Twenty One then purchases at closing. This shows Tether effectively acting as a supplier of Bitcoin liquidity to Twenty One. Going forward, if Tether mines, say, X thousand BTC per year, those coins could be injected into Twenty One either in exchange for more shares or for other consideration. This way, Twenty One can keep growing its BPS without always having to buy in the open market (which could move prices or face competition).

It’s also possible Twenty One might directly invest in or acquire mining operations down the line. Although not stated explicitly, their mandate to “allocate capital to increase Bitcoin per share” could include investing in mining ventures if that yields below-market-cost Bitcoin. Tether’s existing projects could be folded in or co-developed under the Twenty One umbrella. For now, Tether’s mining ensures that some of the Bitcoin backing Twenty One is internally sourced. This is strategically important: it means Twenty One’s fortunes are not solely tied to buying BTC from the market; they are connected to the production side of Bitcoin as well. In a sense, Tether’s mining can be seen as vertical integration for the Twenty One venture – controlling upstream supply of the asset they accumulate.

If Tether eventually does operate one of the largest mining farms, Twenty One stands to benefit by association. One benefit is informational edge: Tether will have granular data on mining economics (costs, hash rate, etc.), which can inform Twenty One’s strategy on when to buy or not buy Bitcoin. For instance, if mining margins are extremely high, Twenty One might conclude the market is bullish and choose to deploy capital faster; or if miners are capitulating, Twenty One might step in to buy distressed assets or cheap BTC. Another benefit is narrative strength: Tether can claim that its Bitcoin in Twenty One is backed not just by purchases but by “sweat equity” – i.e., securing the network via mining. This plays well into Bitcoin community values (support the network that supports you).

However, it’s worth noting that as of the launch, Tether’s mining operations are still ramping up and not yet the absolute largest. Chinese mining pools and a few North American public miners hold that title. Tether’s goal of 450 MW by 2025 would put it in league with top public miners like Marathon Digital (which has tens of exahashes planned, equivalent to a few hundred MW). So Tether isn’t the biggest yet, but it’s on a fast track. This aggressive expansion speaks to Tether’s confidence in Bitcoin’s future – they wouldn’t invest in so much infrastructure if they expected Bitcoin to fade. That confidence is now manifest in Twenty One. Indeed, “With Jack at the helm, we are proud to support this effort to further Bitcoin’s adoption… Twenty One will take a Bitcoin-first approach that aligns with our vision” said Ardoino of Tether. Part of that vision is clearly energy and mining-backed Bitcoin accumulation.

In connecting the dots: Tether mines Bitcoin using renewable energy -> those bitcoins (clean, new coins) can flow into Twenty One’s treasury -> Twenty One’s shareholders benefit from increased BTC holdings -> Twenty One’s public success further legitimizes Bitcoin -> more capital becomes available for Bitcoin mining and investments (completing the cycle). This synergy could make the Tether–Twenty One alliance a self-reinforcing engine in the Bitcoin economy. One could imagine in a few years, Twenty One not only holding, say, 100,000 BTC, but also owning stakes in mining farms producing thousands of BTC annually, making it a hybrid mining-holding conglomerate. For now, the immediate takeaway is that Tether’s mining endeavors complement the Twenty One venture: they both serve the goal of entrenching Bitcoin as a dominant asset, and they feed into each other’s success.

Historical Context and Significance

The emergence of Twenty One Capital can be seen as a culmination of several historical trends in crypto and finance, marking a new chapter in Bitcoin’s institutional journey. To fully appreciate its significance, it’s useful to place it in context:

SPACs and Crypto: The use of a SPAC to launch a crypto-related company comes after a roller-coaster SPAC boom. In 2020–21, SPAC mergers were a popular shortcut to public markets for many tech and fintech companies. Crypto firms joined the fray – for instance, crypto exchange Bakkt went public via SPAC in 2021, and mining companies like Cipher Mining (backed by Bitfury) also did SPAC deals. However, the SPAC boom fizzled by 2022 amid poor post-merger stock performance and greater regulatory scrutiny. Notably, the biggest attempted crypto SPAC, stablecoin issuer Circle (USDC’s parent), had its $9B SPAC deal fall through in late 2022, signaling waning appetite. Against that backdrop, Twenty One’s SPAC merger in 2025 is bold. It indicates that investor appetite for crypto in public markets has rebounded, especially for Bitcoin-focused plays (contrasting with the failure of a stablecoin SPAC). The massive PIPE raise and stock surge on announcement suggest that the market now distinguishes between different kinds of crypto companies – and Bitcoin-first companies may have the upper hand in credibility. Historically, this could be seen as a second wave of crypto listings: the first wave (2019–2022) included miners and exchanges with mixed success; this second wave centers on Bitcoin treasuries and services, perhaps learning from earlier missteps.

Tether’s Evolution: Historically, Tether was a controversial figure – from 2017-2021 it faced doubts about its dollar reserves and had legal clashes (settling with NYAG in 2021 over misrepresentations). By 2023–2024, Tether turned immensely profitable thanks to interest on its reserve assets (U.S. Treasuries) and began diversifying into tangible businesses: mining, payments technology (like investing in Holepunch/Keet for P2P comms), and now this. Twenty One represents Tether’s transition from a shadowy but systemically important stablecoin issuer to a broad-based digital asset conglomerate. It’s almost a redemption arc: Tether leveraging its success (USDT is now ~$145B market cap, making it one of the largest money-market-like funds in the world) to fortify the Bitcoin ecosystem that underpins much of crypto trading. Historically, stablecoins and Bitcoin had a symbiotic but uneasy relationship; Tether is now making that relationship explicit and formal. This could influence other stablecoin issuers – for example, Circle might consider investing more of its reserves in Bitcoin or supporting Bitcoin initiatives to keep pace (especially as an eventual Bitcoin ETF could reduce the need for stablecoins in trading). In the bigger picture of Bitcoin’s evolution, having the largest stablecoin issuer throw its weight fully behind Bitcoin is a major endorsement, likely to be remembered as a turning point where crypto’s foundational companies aligned on Bitcoin maximalism as a strategy.

SoftBank and Fintech: SoftBank’s involvement is historically noteworthy because it has navigated fintech and crypto waters for years. It funded pioneering fintechs (like Paytm, SoFi, Revolut) and dipped into crypto exchanges (FTX, as mentioned). Those bets taught lessons – e.g., FTX’s collapse showed the perils of centralized exchange tokens and poor governance. SoftBank now embracing a Bitcoin-only thesis suggests that after trials in broader crypto, they settled on Bitcoin as the more enduring play. In the annals of SoftBank’s investments, Twenty One might be grouped with its more visionary bets (akin to betting on the internet itself, not just a dot-com). If Twenty One thrives, SoftBank will be seen as having successfully pivoted to a winner in the crypto space, salvaging its earlier missteps. If it fails, it’ll join WeWork and others in SoftBank’s list of over-optimistic bets. But given SoftBank’s influence, its endorsement alone could lead to increased interest from Asia and other SoftBank-affiliated circles in Bitcoin projects. Historically, there’s also an echo here: back in the dot-com boom, Masayoshi Son invested in Yahoo, seeing the promise of the internet. Investing in Twenty One could be seen as seeing the promise of the Bitcoin network as a foundational layer for future finance. It marks one of the first times a major global investment firm has taken a direct equity stake in a company whose primary asset is Bitcoin itself – a sign of Bitcoin’s gradual integration into mainstream high finance.

Jack Mallers and Strike: Jack Mallers’ journey from startup founder to public company CEO symbolizes a generational shift. He represents the cohort of Bitcoin enthusiasts who came of age during the late 2010s, built on Bitcoin’s Lightning Network, and are now stepping onto bigger stages. Historically, Bitcoin’s corporate champions were older figures like Michael Saylor or Jack Dorsey (Block’s CEO), or finance veterans like the Winklevoss twins with their ETF attempts. Mallers is a different breed – very much a product of Bitcoin’s second decade, focusing on remittances and everyday use. His company Strike, launched in 2019, played a pivotal role in demonstrating that Bitcoin’s layer-2 (Lightning) can power real-world payments (e.g., Strike enabled instant low-fee remittances from the US to Mexico by converting dollars to BTC to pesos under the hood). With Strike’s help, El Salvador became the first nation to put Bitcoin on its balance sheet and legalize it, a milestone in 2021. Now, Mallers leading Twenty One in 2025 highlights Bitcoin’s next milestone: integration into global markets and balance sheets at scale via public companies. It’s a sign that the entrepreneurial talent in Bitcoin is maturing and expanding ambitions. If Satoshi Nakamoto and early developers gave Bitcoin life, and figures like Saylor gave it corporate legitimacy, Mallers and peers are the ones building institutions around Bitcoin that could persist for decades. This is important in Bitcoin’s evolution – it’s no longer just a protocol or an asset, it’s spawning entire institutions (like Twenty One) dedicated solely to it.

Bitcoin’s Mainstreaming: Twenty One can be viewed historically alongside other key events that pushed Bitcoin mainstream. Think of the timeline: 2013 saw the first big VC investments in Bitcoin startups, 2016–2017 saw Wall Street dabble (CME futures launched, etc.), 2020 brought MicroStrategy and later Tesla putting Bitcoin on balance sheets, 2021 saw a sovereign nation adopt Bitcoin, 2023-24 were marked by major ETF filings from BlackRock and others. Now, this 2025 event – a Bitcoin-native company formed by a coalition of crypto and Wall Street leaders going public – is another such milestone. It shows the convergence of those prior threads: corporate adoption (treasury holding), institutional investment, and even governmental interest (indirectly, through SoftBank’s global ties and Mallers’ El Salvador experience). The significance is that Bitcoin is no longer just an outsider asset; it is being institutionalized in a novel way. Twenty One could be the first of many “Bitcoin institutions” that are neither traditional banks nor pure crypto startups, but hybrids with traits of both. If successful, this hybrid model could greatly accelerate Bitcoin’s integration such that, by the late 2020s, we might routinely see public companies with major Bitcoin holdings and Bitcoin-based product lines, without anyone raising an eyebrow.

In conclusion, Twenty One Capital’s launch encapsulates the state of Bitcoin in 2025: increasingly accepted, heavily invested in by old and new financial players, and at the center of ambitious plans to reshape finance. It represents a strategic bet that Bitcoin is not just an asset to hold, but a platform on which to build an entire public enterprise. Each key player – Tether, SoftBank, Mallers, Cantor – brings something vital from their historical context: Tether its crypto market dominance and resources, SoftBank its capital and global reach, Mallers his innovation and Lightning-era mindset, and Cantor its Wall Street gravitas and deal-making acumen. Together, they are forging a path that, if it works, could redefine how companies capitalize on Bitcoin and how investors access it. Twenty One’s story will likely be studied in the future as a case of Bitcoin’s financialization – where we went from individuals HODLing coins to institutions structuring multi-billion-dollar ventures around those coins, all while trying to uphold the ethos of decentralization and long-term thinking that Bitcoin inspires.

Whether Twenty One ultimately outperforms the likes of MicroStrategy (and lives up to Mallers’ ambition of being the “most successful company in Bitcoin”) will unfold in time. But its very inception is a bullish indicator for the Bitcoin industry: it signals that key stakeholders are not content with passive adoption; they are proactively engineering the next phase of Bitcoin’s integration into the global financial system, blending the strengths of crypto-native firms and traditional finance. In doing so, they are also taking on the responsibility to educate, advocate, and innovate – factors that could benefit the entire Bitcoin ecosystem beyond just their own profits. The strategic rationale behind Twenty One is thus as much about shaping the future of Bitcoin as it is about reaping returns from Bitcoin. And that perhaps is its most profound implication: Bitcoin is being treated not just as an asset to invest in, but as a foundation to build upon, heralding a new era where public companies might be as native to Bitcoin as they are to dollars.

ERASMUS CROMWELL-SMITH

April 24th. 2025.

Sources:

SEC Filing:

TWENTY ONE PRESS RELEASE: